The World Nuclear Industry Status Report 2013 (HTML)

By

Mycle Schneider

Independent Consultant, Paris, France

Project Coordinator and Lead Author

Antony Froggatt

Independent Consultant, London, U.K.

Lead Author

With

Komei Hosokawa

Professor for Environmental and Social Research, Kyoto Seika University, Japan

Contributing Author

Steve Thomas

Professor for Energy Policy, Greenwich University, U.K.

Contributing Author

Yukio Yamaguchi

Co-director of the Citizen’s Nuclear Information Center (CNIC), Tokyo, Japan

Contributing Author

Julie Hazemann

Director of EnerWebWatch, Paris, France

Documentary Research, Modeling and Graphic Design

Foreword by Peter A. Bradford

Paris, London, July 2013

A Mycle Schneider Consulting Project

Acknowledgments

The project coordinator wishes to thank in particular his colleague, fellow lead author and friend Antony Froggatt for his constant support and extraordinary reliability in this project, and his co-authors Steve Thomas, Komei Hosokawa and Yukio Yamaguchi for their creative special contributions to this report. A big thank you to Peter A. Bradford for his thoughtful foreword.

The authors wish to thank Fred & Alice Stanback, Amory B. Lovins, Rocky Mountain Institute, Rebecca Harms, the Greens-EFA Group in the European Parliament, Arne Jungjohann, Rebecca Bertram, Heinrich Böll Foundation U.S., Sabine von Stockar, the Swiss Renewable Energy Foundation for their generous support for this project.

A big thank you to John Corbett for his extensive research assistance on finances and to Philippe Rivière for his creative work on the website and his generous assistance at any time of the day.

The report has greatly benefitted from partial or full proof-reading, editing suggestions and comments by Aileen Smith, Amory B. Lovins, Miles Goldstick, MV Ramana and Shaun Burnie.

Thank you all.

Special thanks to Anna Jeretic for making available the beautiful artwork and to Adélaïde Dubois-Taine for designing the cover page.

Note. This report contains a very large amount of factual and numerical data. While we do our utmost to verify and double-check, nobody is perfect. The authors are always grateful for corrections and suggestions of improvement.

Lead Authors’ Contacts

Mycle Schneider

45, allée des deux cèdres

91210 Draveil (Paris)

France

Phone: +33-1-69 83 23 79

mycle@orange.fr

Antony Froggatt

53a Nevill Road

London N16 8SW

United Kingdom

Ph: +44-79 68 80 52 99

a.froggatt@btinternet.com

Nuclear power requires obedience, not transparency. The gap between nuclear rhetoric and nuclear reality has been a fundamental impediment to wise energy policy decisions for half a century now. For various reasons in many nations, the nuclear industry cannot tell the truth about its progress, its promise or its perils. Its backers in government and in academia do no better.

Rhetorical excess from opponents of nuclear power contributes to the fog, but proponents have by far the heavier artillery. During the rise and fall of the bubble formerly known as “the nuclear renaissance” in the U.S. many of their tools have been on full display.

Academic and governmental studies a decade ago understated the likely cost of new reactors and overstated their potential contribution to fighting climate change. By 2006 a few U.S. state legislatures had been enticed to expose utility customers to all the risks of building new reactors. Industry-sponsored conferences persuaded businesses and newspapers of an imminent jobs bonanza, ignoring job losses resulting from high electric rates and passing up cheaper, more labor intensive alternatives. These local groups added to the pressure on Congress for more subsidies.

France and Japan were held out as examples of countries that had avoided the timidity and overregulation that had stalled nuclear construction in the U.S. Indeed, it was argued, these nations had even solved the waste problem through their commitment to reprocessing spent fuel.

At times inconsistent tales were told simultaneously. Thus the U.S. Congress was told that the new licensing process and the new generic designs were so untried and environmental opposition so formidable that loan guarantees were needed to lay the risks off on taxpayers. At the same time Wall Street and state legislatures were assured that these new features had chloroformed public opposition and otherwise laid to rest the terrifying industry ghosts embodied by the nine figure dollar losses at Shoreham, Seabrook, WPPSS, and Midland, sites that resonate in U.S. nuclear folklore like Civil War battlefield names.

The renaissance story line was hard to resist. By early 2009, applications for 31 new reactors were pending at the U.S. Nuclear Regulatory Commission. The promises came garnished with tales of remorseful changes of heart from oft-obscure nuclear converts. With few exceptions, the news media - especially television with its thirst for the short and the simple - fell for the renaissance story line.

It is all in ruins now. The 31 proposed reactors are down to four actually being built and a few others lingering on in search of a license, which is good for 20 years. Those four are hopelessly uneconomic but proceed because their state legislatures have committed to finish them as long as a dollar remains to be taken from any electric customer’s pocket. Operating reactors are being closed as uneconomic for the first time in fifteen years.

Still the band plays on. President Obama recently touted new reactors as part of his “all of the above” policy on climate change. But is “all of the above” really a policy? Do we build palaces to avert housing shortages? Don’t we instead prioritize, based on the best information available? U.S. secretaries of energy enthuse that the four new reactors will be completed “on time and on budget”, never mind that they are already behind and over and that “on budget” will mean “well above the cost of creating equivalent low carbon energy more sensibly”.

As always in the face of failure, the industry puts forth new designs as a basis for new promises, now touting small modular reactors with the same fervor that it touted large partially modular reactors a decade ago. Congress finds a few hundred million to preserve these dreams even as its cutbacks shatter so many others.

A new movie, Pandora’s Promise (no filmmaker familiar with nuclear history would include “promise” in a title intended to be pronuclear [1]), recently screened at Sundance.

Featuring the same old converts and straw men, it opened in theaters a few weeks ago to tiny audiences and generally unenthusiastic reviews, especially from reviewers knowledgeable about nuclear power [2].

In the astonishing persistence of the global appetite for false nuclear promises lies the critical importance of the World Nuclear Industry Status Report.

The Report sets forth in painstaking detail the actual experience and achievements of nuclear energy around the world. It is based for the most part on generally accepted data distinctively graphed for clearer understanding. Where the authors introduce judgment, they explain what they have done and why. The Report has a track record stretching back years. It is much better than the embarrassing exuberances of the International Atomic Energy Agency, the World Nuclear Association or the pronouncements of most national governments. If more journalists would use it for reference, their readers would be spared much of the foolishness that they must now consume.

Most of the myths on which the purported nuclear renaissance rested founder on the rocks of the information presented here.

Is new nuclear power cheaper than alternative ways of meeting energy needs? Of course not. What about low carbon “baseload” alternatives? See page 73ff. Can a country grow its economy by building nuclear reactors? What don’t you understand about the employment consequences of imposing rate shock on industrial and commercial customers? Are the consequences of the Fukushima meltowns really being overstated by antinuclear activists? Maybe, but see the chapter on the status of Fukushima.

In short, the nuclear renaissance — whatever it may be called throughout the world — has always consisted entirely of the number of reactors whose excess costs governments were prepared to make mandatory for either customers or taxpayers. Investor capital cannot be conscripted. Investors of the sort that nuclear power must attract study risks carefully. They know the information in this report, and so should everyone else with responsibility for energy decisions that allocate nuclear risk.

[*] Adjunct Professor, Vermont Law School, teaching ’Nuclear Power and Public Policy’, former commissioner U.S. Nuclear Regulatory Commission (NRC), former chair of the New York and Maine Utility Regulatory Commissions.

[1] A more accurate use of the word is in M.V. Ramana’s aptly titled and excellent history of India’s nuclear follies, The Power of Promise (Penguin Viking, 2012).

[2] For an insightful example, see Victor Gilinsky and Henry Sokolski, “Pandora’s Promise: Is the Issue Really Environmental”, Nuclear Intelligence Weekly, June 21, 2013, www.npolicy.org//.

Two years after the Fukushima disaster started unfolding on 11 March 2011, its impact on the global nuclear industry has become increasingly visible. Global electricity generation from nuclear plants dropped by a historic 7 percent in 2012, adding to the record drop of 4 percent in 2011. This World Nuclear Industry Status Report 2013 (WNISR) provides a global overview of the history, the current status and the trends of nuclear power programs worldwide. It looks at nuclear reactor units in operation and under construction. Annex 1 provides 40 pages of detailed country-by-country information. A specific chapter assesses the situation in potential newcomer countries. For the second time, the report looks at the credit-rating performance of some of the major nuclear companies and utilities. A more detailed chapter on the development patterns of renewable energies versus nuclear power is also included. Annex 6 provides an overview table with key data on the world nuclear industry by country.

The 2013 edition of the World Nuclear Industry Status Report also includes an update on nuclear economics as well as an overview of the status, on-site and off-site, of the challenges triggered by the Fukushima disaster. However, this report’s emphasis on recent post-Fukushima developments should not obscure an important fact: as previous editions (see www.WorldNuclearReport.org) detail, the world nuclear industry already faced daunting challenges long before Fukushima, just as the U.S. nuclear power industry had largely collapsed before the 1979 Three Mile Island accident [1]. The nuclear promoters’ invention that a global nuclear renaissance was flourishing until 3/11 [2] is equally false: Fukushima only added to already grave problems, starting with poor economics.

The performance of the nuclear industry over the year from July 2012 to July 2013 can be summed up as follows:

Operation. There are 31 countries operating nuclear power plants in the world. [4] A total of 427 reactors have a combined installed capacity of 364 GWe [5]. These figures assume the final shutdown of the ten reactors at Fukushima-Daiichi and -Daini. It should be noted that as of 1 July 2013 only two (Ohi-3 and -4) of the 44 remaining Japanese reactors are operating and their future is highly uncertain. In fact, even if four utilities are expected to submit restart requests in July 2013, many observers believe that a large share of the suspended Japanese units will likely never restart.

The nuclear industry is in decline: The 427 operating reactors are 17 lower than the peak in in 2002, while, the total installed capacity peaked in 2010 at 375 GWe before declining to the current level, which was last seen a decade ago. Annual nuclear electricity generation reached a maximum in 2006 at 2,660 TWh, then dropped to 2,346 TWh in 2012 (down 7 percent compared to 2011, down 12 percent from 2006). About three-quarters of this decline is due to the situation in Japan [6], but 16 other countries, including the top five nuclear generators, decreased their nuclear generation too.

The nuclear share in the world’s power generation declined steadily from a historic peak of 17 percent in 1993 to about 10 percent in 2012. Nuclear power’s share of global commercial primary energy production plunged to 4.5 percent, a level last seen in 1984. [7] Only one country, the Czech Republic, reached its record nuclear contribution to the electricity mix in 2012.

Age. In the absence of major new-build programs, the unit-weighted average age of the world nuclear reactor fleet continues to increase and in mid-2013 stands at 28 years. Over 190 units (45 percent of total) have operated for 30 years of which 44 have run for 40 years or more.

Construction. Fourteen countries are currently building nuclear power plants, one more than a year ago as the United Arab Emirates (UAE) started construction at Barrakah. The UAE is the first new country in 27 years to have started building a commercial nuclear power plant.

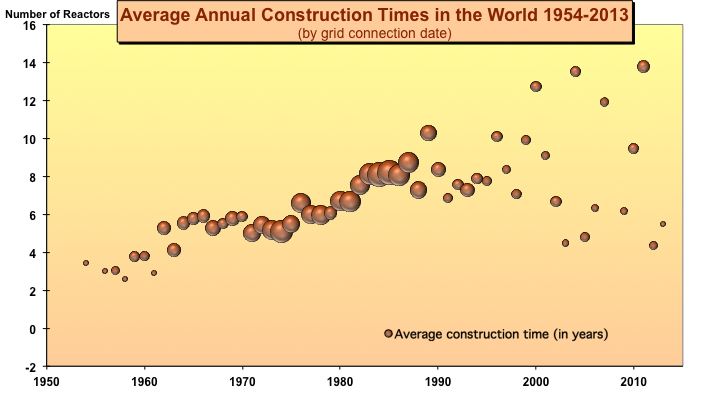

As of July 2013, 66 reactors are under construction (7 more than in July 2012) with a total capacity of 63 GW. The average construction time of the units under construction, as of the end of 2012, is 8 years. However:

• Nine reactors have been listed as “under construction” for more than 20 years and four additional reactors have been listed for 10 years or more.

• Forty-five projects do not have an official planned start-up date on the International Atomic Energy Agency’s (IAEA) database.

• At least 23 have encountered construction delays, most of them multi-year. For the remaining 43 reactor units, either construction began within the past five years or they have not yet reached projected start-up dates, making it difficult or impossible to assess whether they are on schedule or not.

• Two-thirds (44) of the units under construction are located in three countries: China, India and Russia.

The average construction time of the 34 units that started up in the world between 2003 and July 2013 was 9.4 years.

Reactor Status and Nuclear Programs

• Startups and Shutdowns. Only three reactors started up in 2012, while six were shut down [8] and in 2013 up to 1 July, only one started up, while four shutdown decisions—all in the U.S.—were taken in the first half of 2013. [9] Three of those four units faced costly repairs, but one, Kewaunee, Wisconsin, was running well and had received a license renewal just two years ago to operate up to a total of 60 years; it simply became uneconomic to run. As of 1 July 2013, there were only two reactors operating in Japan and how many others will receive permission to restart and over what timeframe remains highly uncertain.

• Newcomer Program Delays. Engagement in nuclear programs has been delayed by most of the potential newcomer countries, including Bangladesh, Belarus, Jordan, Lithuania, Poland, Saudi Arabia and Vietnam.

Construction & New Build Issues

• Construction Cancellation. In Russia, one reactor, which had just started construction in 2012 (Baltic-1), was abandoned in May 2013.

• Construction Starts. In 2012, construction began on six reactors and on three so far in 2013, including on two units in the U.S. for the first time in three and a half decades. Those two units have been offered over $8 billion in federal loan guarantees and other subsidies whose total rivals their construction cost, and special laws have transferred financial risks to the taxpayers and customers.

• Certification Delays. The certification of new reactor designs has continued to be delayed, in the U.S. certification of the Franco-German-designed EPR [10] was pushed back again, this time to 2015. Only the Westinghouse AP1000 has received full generic design approval in the U.S.

• Construction Start Delays. In various countries firmly planned construction starts were delayed, most notably in China, where for almost two years, between December 2010 and November 2012, not a single new reactor building site was opened. Furthermore, in the first half of 2013 it did not start any further constructions.

Economics & Finances

• Capital Cost Increases. Construction costs are a key determinant of the final nuclear electricity generating costs and many projects are significantly over budget. Cost estimates have increased in the past decade from $1,000 to $7,000 per kW installed. The U.S. Vogtle project, now officially under construction, is built by the same firm whose two previous reactors at that site were originally budgeted at $660 million and were later estimated to have cost $9 billion.

• State Aid. The U.K. model of Contract for Difference (CFD), a kind of feed-in tariff agreement for nuclear electricity that is aimed at providing a subsidy scheme for new-build, in the view of many observers, is likely to violate current EU competition rules.

• Operating Cost Increases. In some countries, especially the U.S. illustrated by the Kewaunee case, historically low inflation-adjusted operating costs—especially for major repairs—have escalated so rapidly that the average reactor’s operating costs is barely below the normal band of wholesale power prices.

• Post-Fukushima Costs. Additional costs arising from upgrading and backfitting measures following the lessons of the Fukushima crisis are only beginning to surface. They are likely to have substantial impact on investment as well as operational costs.

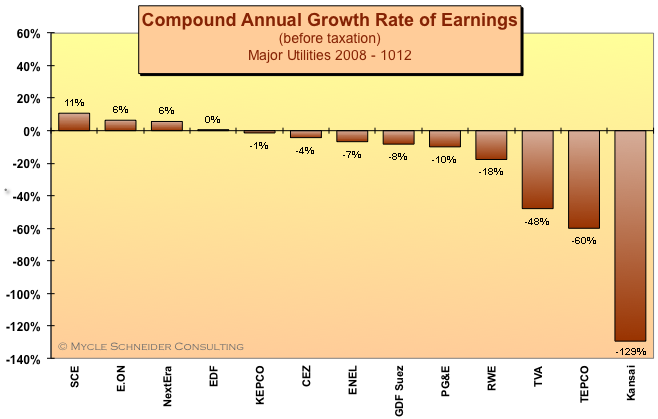

• Income and Debt. Nine out of 14 major utilities assessed saw their earnings decline over the past five years while 13 constantly increased their debt level.

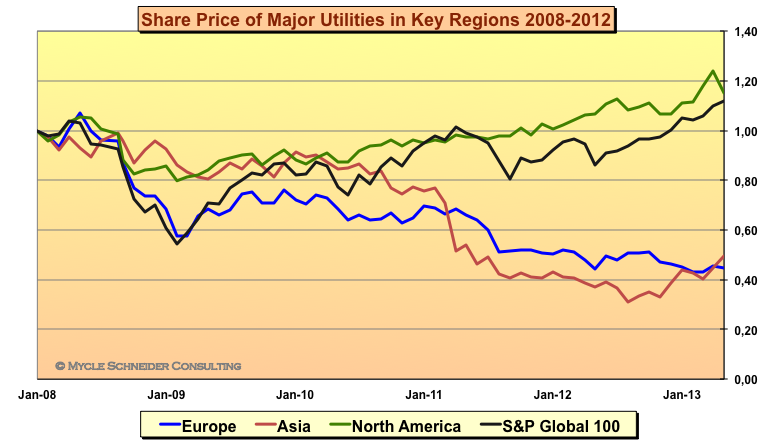

• Credit Rating. Over the past five years, of 15 assessed nuclear utilities, 10 were downgraded by credit rating agency Standard and Poor’s, four companies remained stable, while only one was upgraded over the same period. Rating agencies consider nuclear investment risky and the abandoning of nuclear projects explicitly “credit positive”.

• Share Value. The share value of the world’s largest nuclear operator, French state utility EDF, went down by 85 percent over the past five years, while the share price of the world’s largest nuclear builder, French state company AREVA, dropped by up to 88 percent.

Fukushima Status Report

This assessment includes analyses of on-site and off-site challenges that have arisen from the 3/11 disaster. To what extent the disaster was triggered by the earthquake or the tsunami or by both in combination cannot yet be conclusively elucidated.

• On-site Challenges. Radiation readings inside the reactor buildings of units 1–3 vary between 5 mSv/h and 73 Sv/h [11], which makes human intervention almost impossible. Massive amounts of water, about 360 tons per day, are still pumped into the destroyed reactors via makeshift vinyl tubes that frequently leak. This water, together with a similar additional amount of groundwater, seeps into the basements of the reactor buildings, some of it decontaminated to some degree and re-injected. The amount of radioactive water that cannot be re-used is constantly increasing and has reached 380,000 tons in precarious storage of which 90,000 tons in the basements. It is estimated that 27 times the amount of cesium-137 released into the air in the first three weeks or more than 2.5 times the total amount released at the Chernobyl accident is contained in this water.

• Off-site Challenges. More than 150,000 people remain in forced evacuation. About 130,000 compensation claims have been filed. A total of 101 municipalities in 8 prefectures were designated as a “Scheduled Contamination Survey Zone”, where annual doses between 1 and 20 mSv are predicted and local authorities are responsible for decontamination work. In addition, the central government is in charge of decontamination efforts in 11 municipalities in Fukushima Prefecture covering 235 km2, where annual doses exceed 20 mSv. Less than 5 percent of the surface has seen any decontamination efforts.

The worst-case scenario, as depicted by the Chairman of the Japan Atomic Energy Commission in the middle of the crisis in March 2011, remains the collapse of the spent fuel pool of unit 4 [12] and a subsequent fuel fire, potentially requiring evacuation of up to 10 million people in a 250 km radius of Fukushima, including a significant part of Tokyo.

Nuclear Power vs. Renewable Energy Deployment

In spite of a slight decrease in global investment in 2012, partly reflecting rapidly falling equipment prices, renewable energy development continues its rapid expansion in both, capacity and generation. China, Germany and Japan, three of the world’s four largest economies, as well as India, now generate more power from renewables than from nuclear power.

• Investment. Global investment in renewable energy totaled $268 billion [13] in 2012, down from $300 billion the previous year [14] but still five times the 2004 amount. China increased spending by 20 percent to $65 billion and was by far the largest investor. While some big investors (U.S., Germany, Italy) reduced their spending considerably, some smaller players boosted their investments and reached the top ten, including South Africa, which skyrocketed spending by a factor of 200 to reach $5.5 billion, and Japan, which added 75 percent to reach $16 billion.

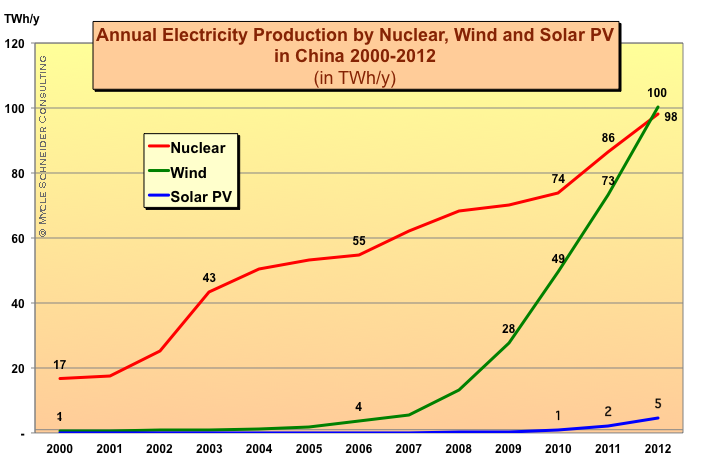

• Installed Capacity. Globally, since 2000, the annual growth rates for onshore wind power have averaged 27 percent and for solar photovoltaics 42 percent. This has resulted in 2012 in 45 GW of wind and 32 GW of solar being installed, compared to a net addition of 1.2 GW of nuclear. China has a total of 75 GW of operating wind power capacity, roughly doubled in each of the past five years.

• Electricity Generation. In 2012 wind produced almost 500 TWh and solar power about 100 TWh more than in 2000, while nuclear power generated 100 TWh less. For the first time in 2012 China and India generated more power from wind than from nuclear plants, while in China solar electricity generation grew by 400 percent in one year.

[1] See Nathan Hultman, Jonathan Koomey, “Three Mile Island: The driver of US nuclear power’s decline”, Bulletin of the Atomic Scientists, May-June 2013, see http://bos.sagepub.com/content/69/3/63, accessed 7 July 2013.

[2] 3/11 refers to the triple disaster earthquake-tsunami-nuclear accident on 11 March 2011.

[3] See Annex 7 for a country-by-country overview of reactors in operation and under construction as well as the nuclear share in electricity generation and primary energy.

[4] Unless otherwise noted, the figures indicated are as of 1 July 2013.

[5] All figures are given for nominal net electricity generating capacity. GW stands for gigawatt or thousand megawatt.

[6] The continuing debacle of the Japanese reactors led to the provisional categorization as “in long-term shutdown”, see main text for details.

[7] According to BP, “Statistical Review of World Energy”, June 2013.

[8] Shutdown is defined as definitively taken off the grid. The shutdown date is the last day when the reactor generated electricity.

[9] The operator decided in June 2013 to shut down the two San Onofre units in California. However, they have not generated electricity for over a year. So in the WNISR database the units have been withdrawn for the year 2012 rather than 2013.

[10] European Pressurized Water Reactor (in Europe) or Evolutionary Pressurized Water Reactor (in the U.S. and elsewhere).

[11] Without massive radiation protection a lethal dose would be reached within minutes.

[12] Pools are above the reactor vessels between the 4th and the 5th floor. The pool of unit 4 contains as much fuel as the 3 others combined.

[13] Does not include any investments in large hydropower projects, but a very small percentage on Carbon Capture and Storage (CCS).

[14] The figure had been corrected upwards from $260 billion after publication of WNISR 2012.

On 29 June 2013, the Director General of the International Atomic Energy Agency (IAEA) declared at the Ministerial Conference in St. Petersburg, Russia that “nuclear power will make a significant and growing contribution to sustainable development in the coming decades”. [1] The future will show whether or not nuclear power will play an increasing role. In the meantime, the World Nuclear Industry Status Report 2013 (WNISR) provides a reality check of the current situation and trends of an industry that in the past has rarely been able to fulfill its own promises. The 2012 edition of the WNISR demonstrated that the IAEA consistently overestimated the development of nuclear power in the world [2], a side-effect of “the leading role of the IAEA in promoting peaceful uses of nuclear energy”. [3]

Contrary to the IAEA’s hopes for the future, this edition of the WNISR shows that nuclear power generation experienced a drop of 7 percent in 2012, larger even than the previous year’s record 4 percent decline. As in previous editions, this report provides many diverse health indicators of the nuclear industry, including numbers of reactors operating, under construction, installed capacities, and extensive country-by-country assessments of nuclear programs around the world. As in the past two editions, a chapter is included that compares certain trends in the nuclear industry with developments in the renewable energy industry.

A greatly extended economic chapter provides data on key strategic markets, especially the U.S. and the U.K., and financial indicators (e.g. share value and credit-rating developments). Professor Steve Thomas once again shares his insights in this area.

In addition, now more than two years after the Fukushima disaster started unfolding, also included is a concise overview of the key issues that continue to raise serious concerns among international experts and the Japanese population. Two independent Japanese experts, Professor Komei Hosokawa from Kyoto and Professor Yukio Yamaguchi from Tokyo have contributed their analysis.

The World Nuclear Industry Status Report has turned into a major international reference on nuclear issues. Over the past year, numerous mainstream publications [4] use the WNISR as their information source for analysis and/or as statistical reference for graphic work, rather than solely relying on IAEA or World Nuclear Association (WNA) data.

The international team that has collaborated to make this project work sincerely hopes that the WNISR 2013 will meet the increasingly high expectations.

[1] International Ministerial Conference, “Nuclear Power in the 21st Century”, St. Petersburg, 27-29 June 2013, Concluding Statement by the President of the Conference, see www.iaea.org//statements/stpclosing.pdf, accessed 30 June 2013.

[2] “Unrealistic Projections”, in Mycle Schneider et al., “World Nuclear Industry Status Report 2012”, see www.worldnuclearreport.org//.

“I would like to begin by congratulating the Kingdom of Swaziland on becoming the 159th Member State of the IAEA.”

Yukiya AmanoIAEA, Director General, Introductory Statement to Board of Governors, 4 March 2013

As of the middle of 2013, a total of 31 countries were operating nuclear fission reactors for energy purposes. Nuclear power plants generated 2,346 terawatt-hours (TWh or billion kilowatt-hours) of electricity in 2012 [1], less than in 1999 and a 172 TWh or 6.8 percent decrease compared to 2011 as well as 11.8 percent below the historic maximum nuclear generation in 2006. The maximum contribution of nuclear power to commercial electricity generation worldwide was reached in 1993 with 17 percent (see figure 1). It has dropped to 10.4 percent in 2012, a level last seen in the 1980s. According to BP, the nuclear share in commercial primary energy consumption dropped to 4.5 percent, “the lowest since 1984”. [2]

Figure 1: Nuclear Electricity Generation in the World

Source : IAEA-PRIS, BP, MSC, 2013

About three-quarters of the decrease is due to the continuing and substantial generation drop in Japan (–139 TWh or –50 percent over the previous year), which in three years fell back from the 3rd to the 18th position of nuclear generators. Production also decreased for differing reasons in all top five nuclear generating countries: United States (–20 TWh or –2.5 percent), France (–16 TWh/–4 percent), Germany (–8 TWh/–10 percent), South Korea (–7 TWh/5 percent) and Russia with an insignificant drop (–0.8 TWh/–0.5 percent).

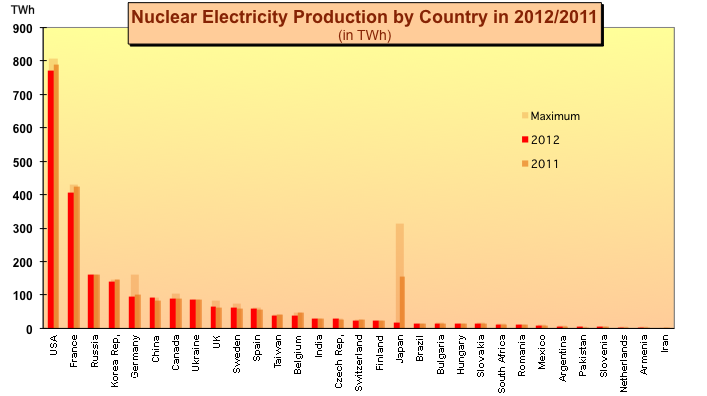

Nuclear generation declined in a total of 17 countries, while in 14 countries it increased or remained stable [3]. Seven countries [4] generated their historic maximum in 2012.

Figure 2. Nuclear Power Generation by Country, 2012/2011 and Historic Maximum

Sources: IAEA-PRIS, MSC, 2013

The “big five” nuclear generating countries—by rank: the United States, France, Russia, South Korea and Germany—generated 67 percent of all nuclear electricity in the world. The three countries that have phased out nuclear power (Italy, Kazakhstan, Lithuania), and Armenia, generated their historic maximum of nuclear electricity in the 1980s. Several other countries’ nuclear power generation peaked in the 1990s, among them Belgium, Canada, Japan, and the U.K. A further six countries peaked their nuclear generation between 2001 and 2005: Bulgaria, France, Germany, South Africa, Spain, and Sweden. Among the countries with a steady increase in nuclear generation are China, the Czech Republic and Russia. However, even where countries are increasing their nuclear electricity production this is in most cases not keeping pace with overall increases in electricity demand leading to a reduced and declining role for nuclear power.

Only one country in the world, the Czech Republic, peaked its nuclear share in 2012 with 35 percent. In fact, all other countries—except Iran, which started up its first nuclear plant in 2011—reached their maximum share of nuclear power prior to 2010. While three countries peaked in 2008 (China) or 2009 (Romania, Russia), the other 26 countries saw their largest nuclear share by 2005. In total, nuclear power played its largest role in ten countries during the 1980s [5], in 12 countries each in the 1990s and in the 2000s.

Increases in nuclear generation are mostly a result of higher productivity and uprating [6] at existing plants rather than due to new reactors. According to the latest assessment by Nuclear Engineering International [7], the global annual load factor [8] of nuclear power plants decreased from 77 percent in 2011 [9] to 70 percent in 2012. Not surprisingly the biggest change was seen in Japan, where the load factor plunged from 69.5 percent in 2010 to 39.5 percent in 2011 to 3.7 percent in 2012. This is also due to the fact that officially 50 of the 54 pre-3/11 units in Japan are still counted as operational—even though some reactors have not generated electricity for years (see box hereunder).

Figure 3. Nuclear Share in Electricity Mix by Country, 2012/2011 and Historic Maximum

Sources: IAEA-PRIS, MSC, 2013

Although both countries decreased performance, as in 2011, Romania and Taiwan had the highest load factors in 2012 with 92.8 and 90.8 percent respectively. The most dramatic reductions in load factor outside Japan were in Belgium (–11.8 percentage points), Mexico (–20 percentage points) and South Korea (–9.5 percentage points). Belgium had two of its seven reactors off-line for much of the year because of thousands of cracks discovered in their pressure vessels. They only restarted in June 2013. Mexico is carrying out major uprating work on both of its units. South Korea had a series of scandals involving quality control issues that kept a number of units down. Other major nuclear countries saw their load factors deteriorate to some degree: the U.S. by 3.1 percentage points to reach 83.2 percent, France by 2.3 percentage points, now down to 73.6 percent and remaining at the lower end of global performance.

Japanese Reactors “in Operation” or “in Long-Term Shutdown”?

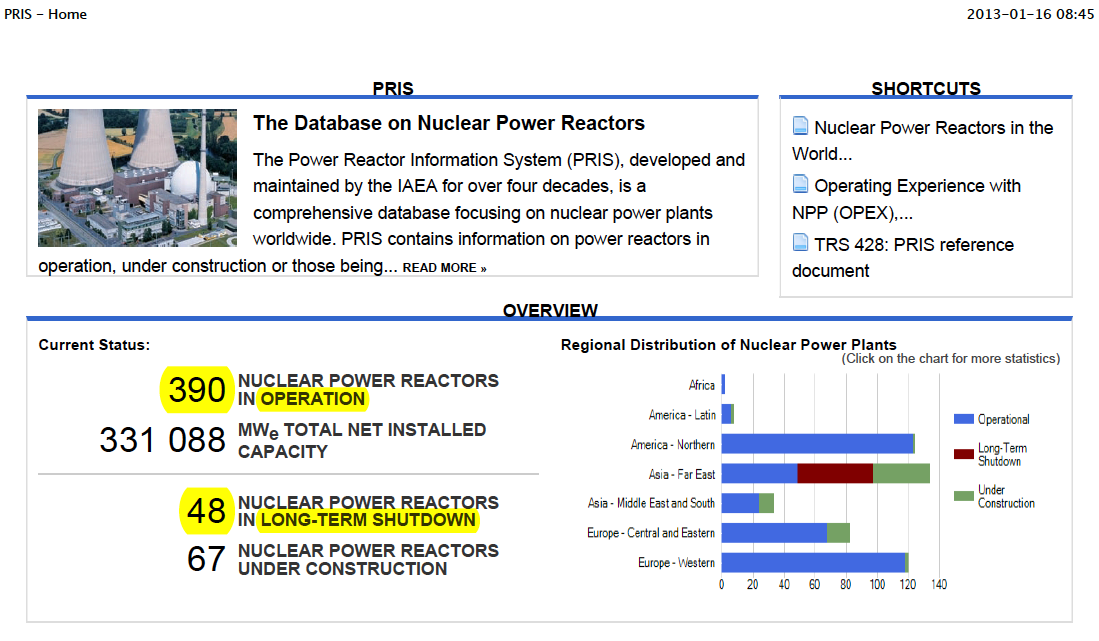

In an unprecedented move, on 16 January 2013, the IAEA shifted 47 Japanese nuclear reactors from the category “In Operation” to the category “Long-term Shutdown” (LTS) in its web-based Power Reactor Information System (PRIS) [10]. The number of nuclear reactors listed as “In Operation” in the world thus dropped to 390, a level last seen in 1986, the year of the Chernobyl accident. The move was a dramatic step by the IAEA in its official statistics by acknowledging the the current industrial reality in Japan. Coming from the IAEA this was without doubt a unique revision of world operational nuclear data.

Screen Capture 1 : The IAEA’s Online Database on Nuclear Power Reactors on 16 January 2013

Note: Yellow highlighting added. Source: IAEA, 2013, see www.iaea.org/pris/

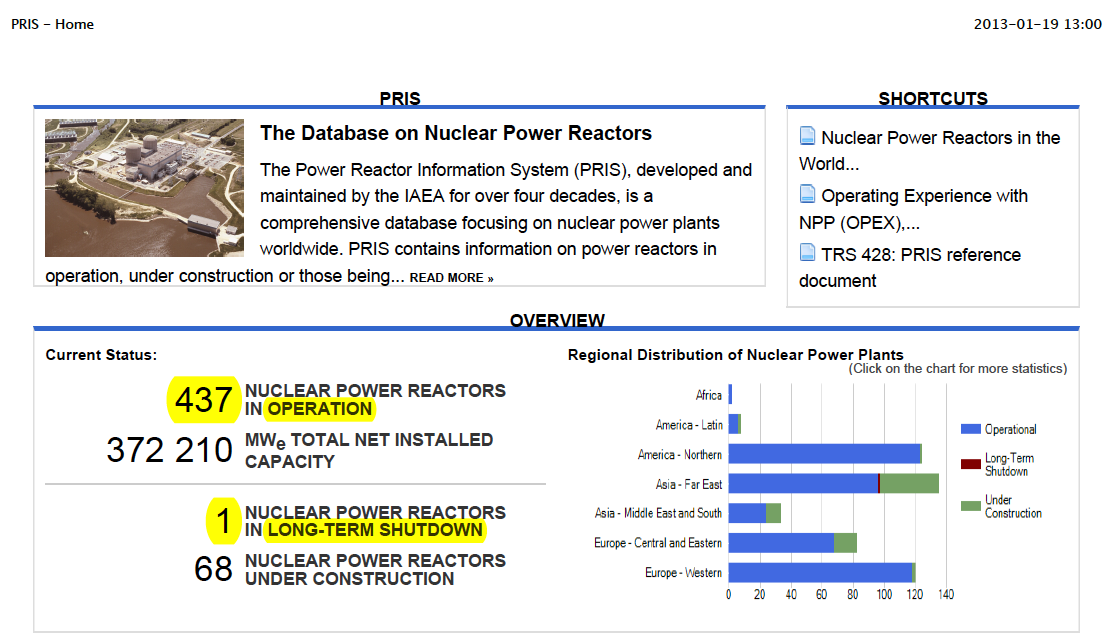

Screen Capture 2 : The IAEA’s Online Database on Nuclear Power Reactors on 19 January 2013

Note: Yellow highlighting added. Source: IAEA, 2013, see www.iaea.org/pris/

This historic revision however, did not last. Only two days later, the Japanese government requested the reversal of the reactor status of the 47 Japanese reactors from the IAEA’s LTS category to “In operation”. The modification was thus reversed on 18 January and commented on by the IAEA in a press release on 19 January 2013. [11]

An IAEA representative explained by email: “In communication with the Government of Japan, it was identified that this status is not applicable for [the] time being and our Japanese counterpart changed the decision and the status was put back.” [12] Another IAEA representative identified the “IAEA counterpart” in a phone interview as the Japan Nuclear Energy Safety Organization (JNES). This was confirmed in the IAEA press release. According to the IAEA, JNES, an incorporated Administrative Agency, modified the raw country data in the online Power Reactor Information System (PRIS) of the IAEA. The modification was then automatically integrated into the World Overview pages of the Agency’s website.

Any correspondent or counterpart to the IAEA’s online database has to be authorized by its respective government. In addition, it is understood that modifications of the reactor status are controlled by the respective government. However, it is unclear what happened in this case, as it is hard to believe that such a significant modification of the reactor status of the Japanese reactor fleet happened at the initiative of an individual at JNES. If this was indeed the case, the question remains why this was done. The IAEA stated that the Japanese counterparts advised the Agency that the “changes resulted from a clerical error”.

The explanation given of a “clerical error” is surprising and unconvincing. The reactor-by-reactor changes were precise and made perfect sense. In fact, all of the 47 reactors could well fall within the IAEA definition for LTS status [13]:

Reactor is considered in long-term shutdown status from the Long-term Shutdown date to the Restart Date, if it has been shut down for an extended period (usually more than one year) and any of the following conditions has occurred in early period of shutdown:

1. restart is not being aggressively pursued (there is no vigorous onsite activity to restart the unit) or

2. no firm restart date or recovery schedule has been established, but there is the intention to re-start the unit eventually.

This status may be for example due to technical, economical, strategic or political reasons. This status does not apply to long-term maintenance outages, including unit refurbishment, if the outage schedule is consistently followed, or to long-term outages due to regulatory restrictions (licence suspension), if restart (licence recovery) term and conditions have been established. Such units are still considered ‘operational’ (in a long-term outage).

If an intention not to restart the shutdown unit has been officially announced by the owner, the unit is considered ‘permanently shut-down’.

Furthermore, if this incident was due to a simple “clerical error”, why would it take JNES two days to notify the Agency?

The incident raises the question of the operational rules of the PRIS database. It seems astounding that representatives of individual governments, utilities, research or safety organizations can actually directly modify the IAEA’s public website. The IAEA explained that it “runs the PRIS database with input from its Member States, which own the information provided”. However, as a consequence of the Japan incident, the Agency decided to change the procedures [14]:

The Nuclear Energy Department of the IAEA, which runs the PRIS database, is implementing a software upgrade that in future would prevent status changes being entered into the system without the agreement of the system administrators, and would require clear justification from the national counterparts.

Any outside observer would have expected this to be the rule before the incident. The overall information management by the IAEA and the Japanese authorities—with very significant changes in reactor statistics, one way or the other, without any public explanation for three days—puts serious doubts on the reliability of the information provided.

Overview of Operation, Power Generation, Age Distribution

Since the start of the commercial nuclear power age in the mid-1950s there have been two major waves of grid connections (see Figure 4). A first wave peaked in 1974, with 26 reactor startups in that year. The second wave reached a historic maximum in 1984 and 1985, just before the Chernobyl accident, reaching 33 grid connections in each year. By the end of the 1980s, the uninterrupted net increase of operating units had ceased, and in 1990 for the first time the number of reactor shutdowns outweighed the number of startups. The 1992-2001 decade showed twice as many startups than shutdowns (51/23), while in the past decade 2003-2012 the trend reversed (31/51). Six reactors (including two units at San Onofre, California, that did not generate any power anymore in 2013) were shut down in 2012, while only three started up. In the first half of 2013, another two units were closed (also in the U.S.), while only one unit started up (in China).

Figure 4. Nuclear Power Reactor Grid Connections and Shutdowns, 1956–2013

Source: IAEA-PRIS, MSC, 2013

As of 1 July 2013, under the Baseline Scenario (see hereunder), a total of 427 nuclear reactors were considered operating in 31 countries, down 17 from the maximum of 444 in 2002. The current world reactor fleet has a total nominal electric net capacity of about 364 gigawatts (GW or thousand megawatts). However, there are large uncertainties in these figures, mainly stemming from the undefined future of the 50 Japanese nuclear reactors that are officially still operating but, except for two units, are all shut down as of 1 July 2013. We have therefore considered three scenarios:

• The Baseline Scenario. Only the 10 Fukushima reactors are permanently closed. Many industry analysts now consider this as unrealistically optimistic. However, it remains unclear, which units will remain closed. Utilities were awaiting the Nuclear Regulatory Authority’s new safety rules that were released on 8 July 2013. Four utilities have announced “early applications for restart” for 10 reactors [15], whatever that means in practice.

• The East Coast Scenario. In addition to the Fukushima units, the seven reactors affected directly or indirectly by 3/11 events remain closed. These include three Onagawa reactors that were closest to the 3/11 epicenter, the three remaining Hamaoka units shut down at the request of former Prime Minister Naoto Kan because of high earthquake risk estimates and the Tokai reactor, the nuclear plant closest to the Tokyo Metropolitan area (ca. 100 km). Under this scenario, the total number of operating units in the world would drop to 420 and the installed capacity to 354 GWe.

• The German Scenario. In addition to the units considered closed under the Baseline and East Coast Scenarios the 13 reactors in Japan with an operational age in excess of 30 years will remain shut down. The German government decided in the wake of 3/11 to permanently shut down the eight reactors down that had operated for over three decades. That would leave Japan with 24 operating reactors, the worldwide figure would drop to 407, last seen in 1987, and the installed capacity to 349 GWe, not experienced since the mid-1990s.

Figure 5. World Nuclear Reactor Fleet, 1954–2013

Sources: IAEA-PRIS, MSC, 2013

Considering the opposition to nuclear power in Japan, especially by local authorities under the influence of an increasingly vocal public opinion, against the restart of any nuclear reactor, it is possible—even under a strongly pro-nuclear central government—that there will be the short-term closure of the majority of the nuclear program in the country. This would not be a “phase-out” scenario but rather the simple “abandoning” of nuclear power. Every authorization of restart will be subject to intense battles between promoters and opponents of the nuclear option. The continuous instability of the Fukushima site could also lead to further incidents and additional releases of large amounts of radioactivity, especially following strong aftershocks, of which a substantial risk persists. Under these circumstances, the scenarios above are likely to prove quite conservative.

The total world installed nuclear capacity has decreased six times since the beginning of the commercial application of nuclear fission, all in the past 15 years—in 1997, 2003, 2007, 2008, 2009 and 2011. Despite 15 fewer units operating in early 2012 compared to 2002, the generating capacity is still about identical and as of late June 2013, with two fewer units operating, the installed capacity is identical to its value a year ago. This is a result of the combined effects of larger units replacing smaller ones and, mainly, technical alterations at existing plants, a process known as uprating. In the United States, the Nuclear Regulatory Commission (NRC) has approved 148 uprates since 1977. These included, in 2012, six uprates between 1.6 percent (Harris 1) and 13.1 percent (Grand Gulf 1). The cumulative approved uprates in the United States total 6.9 GW. [16] Most of these have already been implemented. A similar trend of uprates and lifetime extensions of existing reactors can be seen in Europe. The main incentive for lifetime extensions is their considerable economic advantage over new-build, but upgrading and extending the operating lives of older reactors have lower safety margins than replacement with more modern designs.

It appears however that the incentives for power uprates are waning as in 2012 the number of units with pending applications dropped from 20 in the previous year to 14 and the total capacity increase that would occur from 1.5 GW to 1 GW. [17] The increasing challenge for existing U.S. reactors to compete with wholesale market prices set by the operating costs of gas-fired and wind generators led nuclear giant Exelon to abandon planned uprates for four older units. [18]

Adding together uprates, new-build capacity, and substracting closures, the capacity of the global nuclear fleet increased by about 30 GWe between 1992 and 2002 to reach 362 GWe; it peaked in 2010 at 375 GWe before falling back to the level achieved a decade ago.

The use of nuclear energy has been limited to a small number of countries, with only 31 countries, or 16 percent of the 193 members of the United Nations, operating nuclear power plants in early 2013 (see Figure 2). Half of the world’s nuclear countries are located in the European Union (EU), and in 2012 they accounted for 36 percent of the world’s nuclear production. France alone generated about half (48 percent) of the EU’s nuclear production.

Overview of Current New Build

Currently, 14 countries are building nuclear power plants. With the United Arab Emirates (UAE) concreting the base-slab for two units at Barakah in July 2012 and May 2013, one country was added to the list compared to the last edition of the WNISR. Japan halted work at two units following the 3/11 events, Ohma and Shimane-3, which had been under construction since 2007 and 2010 respectively. Officially construction resumed at Ohma on 1 October 2012 and Shimane-3 has remained “under construction”, according to Japan Atomic Industrial Forum (JAIF) [19] and IAEA statistics. However, in view of the current situation in Japan, we consider it very unlikely that these plants will be completed; it will be hard enough for the industry to get its stranded plant restarted.

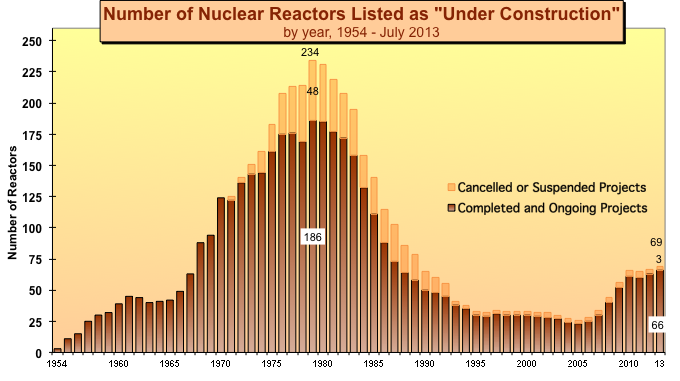

In the previous WNISR edition, the Russian Kursk-5 unit was removed from the list, following reports that the builder, Rosatom, confirmed that the project was abandoned. The unit finally disappeared from the IAEA’s data base early July 2013. So, as of early July 2013, 66 reactors are defined here as under construction, seven more than a year ago. However, 28 of these are in China, leaving the total in the rest of the world being 38. The current number compares with a peak of 234 units in building progress—totaling more than 200 GW—in 1979. However, many of those projects (48) were never finished (see Figure 6.) The year 2004, with 26 units under construction, marked a record low for construction since the beginning of the nuclear age in the 1950s.

After a near two year freeze on nuclear plant construction following the events of March 2011, when no new building site was opened, China resumed construction on 17 November 2012. [20] The World Nuclear Association assumes that at least five authorized construction starts did not happen, with at least another ten in the pipeline for 2011 alone. [21]

Figure 6. Number of Nuclear Reactors under Construction

Source: IAEA-PRIS, MSC 2013

The total capacity of units now under construction in the world is about 63 GWe, up by about 7 GWe compared to a year ago, with an average unit size of 960 MW (see Table 1 and Annex 7 for details). A closer look at currently listed projects illustrates the level of uncertainty associated with reactor building, especially given that most constructors assume a five-year construction period:

Nine reactors have been listed as “under construction” for more than 20 years. The U.S. Watts Bar-2 project in Tennessee holds the record, as construction started in December 1972, but was subsequently frozen. It failed to meet the latest startup date in 2012 and is now scheduled to be connected to the grid in 2015. Other long-term construction projects include three Russian units, two Mochovce units in Slovakia, and two Khmelnitski units in Ukraine. The construction of the Argentinian Atucha-2 reactor started 32 years ago.

Four reactors have been listed as “under-construction” for over 10 years. These are two Taiwanese units at Lungmen for about 14 years and two Indian units at Kudankulam for around 10 years.

Forty-five projects do not have an IAEA planned start-up date.

At least 23 of the units listed by the IAEA as “under construction” have encountered construction delays, most of them significant. All of the 43 remaining units were started within the last five years or have not reached projected start-up dates yet. This makes it difficult to assess whether or not they are on schedule.

Two thirds (44) of the units under construction are located in just three countries: China, India and Russia. Historically, none of these countries have historically been very transparent or reliable about information on the status of their construction sites. It is nevertheless known that half of the Russian units listed are experiencing multi-year delays (see Annex 7 for details).

Table 1: Nuclear Reactors “Under Construction” (as of 1 July 2013) [22]

Country

Units

MWe (net)

Construction Start

Grid Connection

China

28

27,790

2008-2013

2013-2017

Russia

9

7,273

1983-2019

2014-2019

India

7

4,824

2002-2011

2013-2016

South Korea

5

6,320

2008-2013

2013-2017

USA

3

3,399

1972-2013

2015-2017

Pakistan

2

630

2011

2016-2017

Slovakia

2

880

1985

2014-2015

Taiwan

2

2,600

1999

2014-2015

UAE

2

2,690

2012-2013

2017-2018

Ukraine

2

1,900

1986-1987

2015-2016

Argentina

1

692

1981

2013

Brazil

1

1,245

2010

2016

Finland

1

1,600

2005

2016

France

1

1,600

2007

2016

Total

66

63,443

1972-2013

2013-2019

Source : IAEA-PRIS, MSC, 2013

The lead time for nuclear plants includes not only construction times but also lengthy licensing procedures in most countries, complex financing negotiations, and site preparation.

Past experience shows that simply having an order for a reactor, or even having a nuclear plant at an advanced stage of construction, is no guarantee for grid connection and power production. The French Atomic Energy Commission (CEA) statistics on “cancelled orders” through 2002 indicate 253 cancelled orders in 31 countries, many of them at an advanced construction stage (see also Figure 6). The United States alone accounted for 138 of these cancellations. [23] Many U.S. utilities incurred significant financial harm because of cancelled reactor-building projects.

Operating Age

In the absence of any significant new-build and grid connection over many years, the average age (since grid connection) of operating nuclear power plants has been increasing steadily and now stands at about 28 years. [24] Some nuclear utilities envisage average reactor lifetimes of beyond 40 years and even up to 60 years. In the United States, reactors are initially licensed to operate for 40 years. Nuclear operators can request a license renewal for an additional 20 years from the NRC. As of June 2013, 72 of the 100 operating U.S. units have received an extension, and another 18 applications are under NRC review. [25] However, these applications are currently on hold pending completion of a review of the management of commercial nuclear reactor spent fuel, with no license extension decision to be granted until completion of this process. [26]

Even license renewal does not guarantee longer operating life. None of the 32 units that have been shut down in the U.S. had reached 40 years on the grid. In other words, at least a quarter of the reactors built in the U.S. never reached their design lifetime. On the other hand, of the 100 currently operating plants 24 units have operated for 40 years or more.

Many other countries, however, have no time limitations on operating licenses. In France, where the country’s first operating PWR started up in 1977, reactors must undergo in-depth inspection and testing every decade. The French Nuclear Safety Authority (ASN) evaluates on a reactor-by-reactor basis whether a unit can operate for more than 30 years. At this point, ASN considers the issue of lifetimes beyond 40 years to be irrelevant, although the French utility EDF has clearly stated that, for economic reasons, it plans to prioritize lifetime extension over large-scale new-build. However, only a few plants have so far received a permit to extend their operational life from 30 to 40 years, but only under the condition of significant upgrading. President François Hollande vowed to close down the country’s oldest reactors at Fessenheim by the end of 2016 and to engage on a path leading to the reduction of the nuclear share in power generation from 75 to 50 percent by 2025. These decisions were confirmed in September 2012 by the Conseil de Politique Nucléaire, the highest nuclear decision-making body chaired by the President himself. [27] However, even if ASN gave the go-ahead for all of the oldest units to operate for 40 years, 22 of the 58 French operating reactors will reach that age by 2020.

Figure 7. Age Distribution of Operating Nuclear Reactors, 2013

Sources: IAEA-PRIS, MSC, 2013

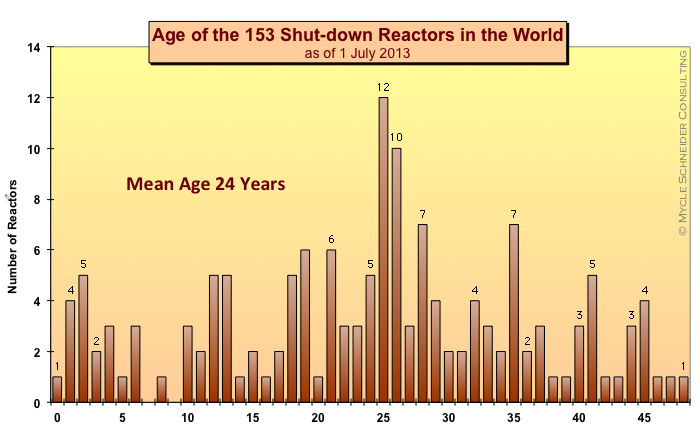

In assessing the likelihood of reactors being able to operate for up to 60 years, it is useful to compare the age distribution of reactors that are currently operating with those that have already shut down (see Figures 7 and 8). As of mid-2013, 31 of the world’s operating reactors have exceeded the 40-year mark. [28] As the age pyramid illustrates, that number will rapidly increase over the next few years. A total of 190 units have already reached age 30 or more.

The age structure of the 153 units already shut down confirms the picture. In total, 47 of these units operated for 30 years or more and of those, 20 reactors operated for 40 years or more (see Figure 8). The majority of these were Magnox reactors located in the U.K. As they were designed to produce weapons-grade plutonium, these were all small reactors (50–490 MW) that had operated with very low burn-up fuel and very low power density (watts of heat per liter of core volume). Therefore there are significant differences from the large 900 MW or 1,300 MW commercial reactors whose high burn-up fuel and high power density generate significantly more stress on materials and equipment. Many units of the first generation have operated for only a few years. Considering that the average age of the 153 units that have already shut down is about 24 years—with 8 more units shut down over the past year the figure did not change—plans to extend the operational lifetime of large numbers of units to 40 years and beyond seem rather optimistic.

As a result of the Fukushima nuclear disaster questions have been raised about the wisdom of operating older reactors. The Fukushima-I units (1 to 4) were connected to the grid between 1971 and 1974. The license for unit 1 was extended for another 10 years in February 2011. Four days after the accidents in Japan, the German government ordered the shutdown of seven reactors that had started up before 1981. These reactors, together with another unit that was closed at the time, never restarted. The sole selection criterion was operational age. Other countries did not adopt the same approach, but it is clear that the 3/11 events had an impact on previously assumed extended lifetimes in other countries as well, including in Belgium, Switzerland and Taiwan.

Figure 8. Age Distribution of Shutdown Nuclear Reactors, 2013

Sources: IAEA-PRIS, MSC, 2013

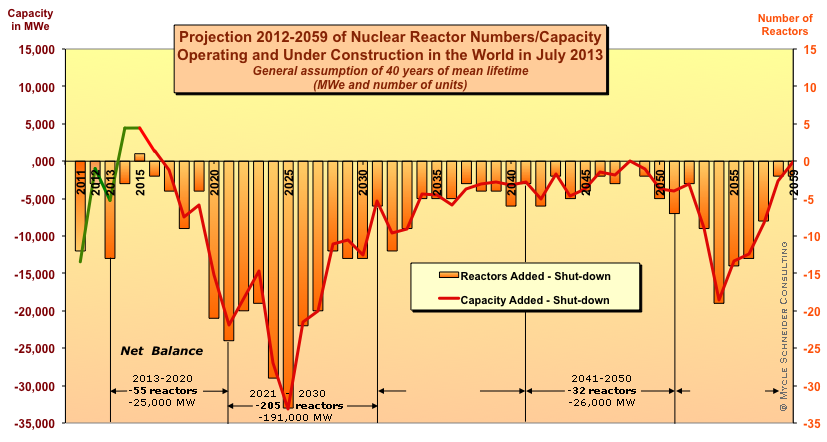

For the purposes of capacity projections, in a first scenario (40-Year Lifetime Projection, see Figure 9), we have assumed a general lifetime of 40 years for worldwide operating reactors, with a few adjustments, while we take into account already-authorized lifetime extensions in a second scenario (PLEX Projection). There are several individual cases where continued operation or lifetime extensions are in question and an official decision to shutdown earlier has been made [29] (see Figure 10).

The lifetime projections make possible an evaluation of the number of plants that would have to come on line over the next decades to offset closures and simply maintain the same number of operating plants. Even with 66 units under construction—as of 1 July 2013, all of which are considered online by 2020—installed nuclear capacity would drop by 25 GW. Therefore in total 55 additional reactors would have to be finished and started up prior to 2020 in order to maintain the status quo. This corresponds to between eight and nine new grid connections per year, with an additional 205 units (191 GW) over the following 10-year period—one every 18 days. This compares to 33 grid connections over the past 10-year period.

Figure 9. The 40-Year Lifetime Projection

Sources: IAEA-PRIS, WNA, MSC 2013

The achievement of the 2020 target appears increasingly unlikely given the existing difficult financial situation of the world’s main reactor builders and utilities, the general economic crisis and generally hostile public opinion—aside from any other specific post-Fukushima effects. A notable difference to previous assessments consists in the assumption that constraints on the manufacturing of key reactor components is playing a minor role as reactor orders have not been following capacity extensions, in particular of key component manufacturer Japan Steel Works (JSW).

As a result, the number of reactors in operation will decline over the coming years unless lifetime extensions beyond 40 years becomes widespread. The scenario of such generalized lifetime extensions is however even less likely after Fukushima, as many questions regarding safety upgrades, maintenance costs, and other issues would need to be much more carefully addressed.

Developments in Asia, and particularly in China, do not fundamentally change the global picture. Reported figures for China’s 2020 target for installed nuclear capacity have fluctuated between 40 GW and 120 GW in the past. The freeze of construction initiation for almost two years has reduced Chinese ambitions. While there has been considerable acceleration of construction starts in the past—with 19 new building sites initiated in 2009 and 2010—not a single new construction site was initiated between December 2010 and November 2012, and none was reported in the first half of 2013. In addition, the average construction time for the 18 operating units in China was 5.8 years. At present, 28 units with about 28 GW are under construction and scheduled to be connected before 2018, which will bring the total to 42 GW. The prospects for significantly exceeding the original 2008 target of 40 GW for 2020 is unlikely. There are also indications that new reactors will be allowed only in coastal, not inland, sites, restricting the number of suitable sites available.

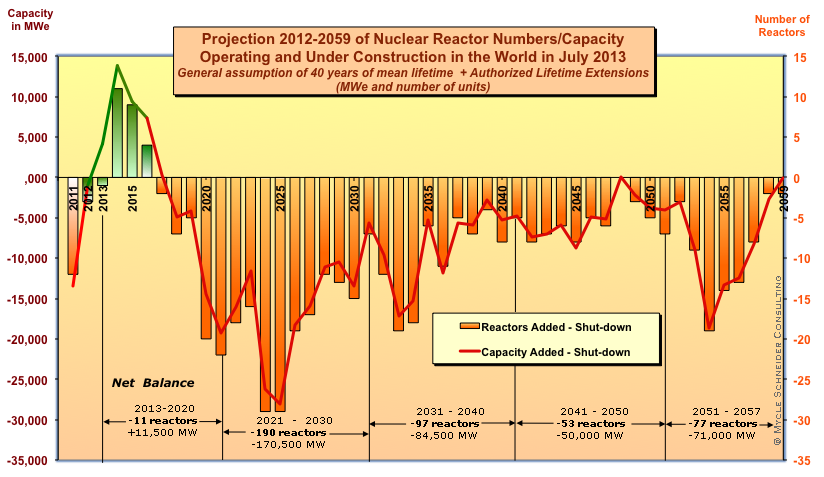

We have also modeled a scenario in which all currently licensed lifetime extensions and license renewals (mainly in the United States) are maintained and all construction sites are completed. For all other units we have maintained a 40-year lifetime projection, unless a firm earlier or later shutdown date has been announced. The net number of operating reactors would still decrease by 11 units even if installed capacity would grow by 11.5 GW in 2020. The overall pattern of the decline would hardly be altered, it would merely be delayed by some years. (See Figures 10 and 11).

Figure 10. The PLEX Projection

Sources: IAEA-PRIS, US-NRC, WNA, MSC 2013

Figure 11. Forty-Year Lifetime Projection versus PLEX Projection (in numbers of reactors)

Sources: IAEA-PRIS, US-NRC, MSC 2013

[1] If not otherwise noted, all nuclear capacity and electricity generation figures based on International Atomic Energy Agency (IAEA), Power Reactor Information System (PRIS) online database, www.iaea.org/programmes/a2/index.html.

[2] BP, “Statistical Review of World Energy”, June 2013.

[3] Less than 1 TWh variation from the previous year

[4] Brazil, China, Czech Republic, Hungary, India, Iran, Pakistan

[5] Armenia, Hungary, India, Germany, Italy, Netherlands, South Africa, South Korea, Spain, Taiwan.

[6] Increasing the capacity of nuclear reactors by equipment upgrades e.g. more powerful steam generators or turbines.

[7] Nuclear Engineering International, “Load Factors to end December 2012”, May 2013.

[8] Nuclear Engineering International load factor definition: “Annual load factors are calculated by dividing the gross generation of a reactor in a one-year period by the gross capacity of the reactor (sometimes called output), as originally designed, multiplied by the number of hours in the calendar year. The figures are expressed as percentages. Where a plant is uprated, the revised capacity is used from the date of the uprating.”

[9] NEI revised the 2011 figure from 76 to 77 percent.

[12] Email to Mycle Schneider, dated 18 January 2013 as a reply to our request from 16 January, prior to the release of the first story on the issue on www.WorldNuclearReport.org, “Historic Move: IAEA Shifts 47 Japanese Reactors Into ‘Long-Term Shutdown’ Category”, 16 January 2013, see www.worldnuclearreport.org//.

[23] CEA, “Elecnuc – Nuclear Power Plants in the World”, 2002.

[24] Here, reactor age is calculated from grid connection to final disconnection from the grid. In this report, “startup” is synonymous with grid connection and “shutdown” with withdrawal from the grid.

[28] We count the age starting with grid connection, and figures are rounded by half-years.

[29] The Japanese reactors constitute the largest contingency of uncertainty. In this scenario all but the 10 Fukushima reactors would return to operation. A highly conservative assumption.

In its International Status and Prospects for Nuclear Power 2012 [1] the IAEA estimates that there are a total of 29 countries that are described as developing nuclear power programs for the first time. This includes three countries that have ordered nuclear power plants, 14 countries that are considering starting a nuclear power program and in which there is a “strong indication of intentions to proceed”, six countries show “active preparation for a possible nuclear power program” and a further six that are actively preparing for a possible nuclear power program with no final decision. The total number of countries listed as developing nuclear power programs has fallen since the IAEA last published its assessment in 2010, when there were 33.

According to the IAEA, the three countries that have ordered nuclear power plants are the United Arab Emirates (UAE), Turkey and Belarus. The Agency also states that there are nine countries that have suggested a start-up date for first power before 2030. The IAEA does not list those countries, but it is likely to include the three in which orders have been placed, plus Bangladesh, Jordan, Lithuania, Poland, Saudi Arabia and Vietnam. This 2012 analysis from the IAEA is a retreat from its suggestions earlier in the same year when it stated it expected Vietnam, Bangladesh, United Arab Emirates, Turkey and Belarus to start building their first nuclear power plants in 2012 and that Jordan and Saudi Arabia could follow in 2013. [2] This prediction seems to be divergent with actual events, with only the UAE starting construction, one unit each in 2012 and 2013. IAEA Director General Yukiya Amano reported to his Board of Governors in March 2013: “The UAE is the first new country in 27 years to have started building a nuclear power plant.” [3]

Figure 12 illustrates the history of national nuclear programs with the startup of the first and shutdown of the last reactor per country.

Figure 12. Start-ups and Closures of National Nuclear Power Programs, 1950–2013

Sources: IAEA-PRIS 2013, MSC, 2013

Below is an assessment by country of the status of the projects that the IAEA has referred to, which indicates that most are much further from the launch of their program than the IAEA frequently suggests.

Bangladesh currently has an installed electricity capacity of 6 GW, with plans to introduce an additional 20 GW by 2020, reportedly to service the 60 percent of the population lacking access to electricity. [4] Bangladesh has been considering embarking on nuclear power for 50 years [5] and the latest attempt is expected to come from 2 GW of nuclear provided by Russian reactors. In 2011 Science Minister Yeafesh Osman was quoted as saying “we have signed the deal… to ease the power crisis”. He said that construction of the plants would start by 2013 and would take five years to complete. [6] In January 2013 Deputy Finance Minister of Russia Sergey Storchak and Economic Relations Division (ERD) Secretary of Bangladesh Md Abul Kalam Azad signed an agreement on the Extension of State Export Credit for financing the preparatory stage work at Rooppur. [7] However, the deal is only for $500 million [8] and will only cover the site preparatory work. [9] According to Rosatom this will begin in January 2014 [10] and is being complemented with $150 million of domestic financing. Completion of this phase is expected by June 2017. [11]Nuclear Intelligence Weekly suggests that groundwork will only start in January 2015 and startup by 2018. [12]

As with many other countries, access to water has been identified as a potential stumbling block of the Rooppur (or Ruppur) plant, with plans to site it on the banks of the river Padmar. During the first half of the year, much of the river’s water resource is already withdrawn by India through the Farakka Barrage, leaving insufficient cooling water for the plant and other activities in Bangladesh. [13]

In mid-2006, the government of Belarus, which, 20 years before, was heavily contaminated by the Chernobyl accident, approved a plan for construction of a nuclear power plant in the Mogilev region in the east of the country. An agreement with Russia on cooperation for the construction of a nuclear power plant in Belarus was signed on 15 March 2011. Expressions of interest were sought from international companies, and, not surprisingly given the existing economic and political ties, a bid from Russia’s Atomstroyexport was taken forward. Under a financing agreement, Russia would provide a $9 billion loan. Prior to 3/11, the two countries reportedly aimed at the signature of an agreement on plant construction in spring 2011, with construction starting in September of the same year. [14] In November 2011 it was agreed that Russia would lend up to $10 billion for 25 years to finance 90 percent of the contract between Atomstroyexport and the Belarus Directorate for Nuclear Power Plant Construction. In February 2012 Russian state-owned Vnesheconombank (VEB) and Belarusian commercial bank Belvnesheconombank signed an agreement to implement the Russian export credit facility. [15] In July 2012 a contract was signed for the construction of two VVER 1200 reactors (analogous to the Western PWR), with an estimated cost of $10 billion, including a $3 billion in infrastructure costs to accommodate the undeveloped remoteness of Ostrovets in northern Belarus. [16] In December 2012, Russian Vnesheconombank authorized allocating a $500 million credit line for the Belarusian Finance Ministry to make advance payments for preparation work [17]. This phase was scheduled to be completed by mid-2013 with concreting work to start in September 2013. The first unit is scheduled to be operational in 2017. [18]

In August 2011, the Ministry of Natural Resources and Environmental Protection of Belarus stated that the first unit would be commissioned in 2016 and the second one in 2018. Both would be of the VVER “NPP-2006” type with a capacity of 1170 MW each. [19] However, it is now expected that the reactors will not be completed until 2018 and 2020. [20] Opposition to the project is increasing. On the 26th anniversary of the Chernobyl catastrophe in 2012, about one-thousand people demonstrated in the Belarussian capital Minsk against the nuclear project, [21] with a similar sized protest held in April 2013 [22].

The Lithuanian Government has repeatedly criticised the safety of the project and has particular concerns as the proposed site at Astravyets as it is only 50 km from its capital Vilnius. The Espoo Convention Implementation Committee has instructed Belarus to continue environmental impact assessment procedures based on the Espoo Convention in order to provide answers to all the questions asked by Lithuania and take into consideration all comments. However, Vitalijus Auglys, director of the Pollution Prevention Department in Lithuania’s Natural Resources Ministry, stated: “We haven’t received the latest information from them. We can’t even start consultations with them, because we must hold public discussions.” [23]

Lithuania had two large RMBK (Chernobyl-type) reactors at Ignalina which were shut down in 2004 and 2009 as part of the agreement to join the European Union. Before the 2009 shutdown, Lithuania’s remaining unit generated 76.2 percent of the country’s electricity, the largest percentage share worldwide. As a result of the closure, Lithuania has significantly increased electricity imports from Belarus, Latvia and Russia. The decision to boost electricity imports is purely based on economic considerations. By the end of 2011, the country had an installed capacity of about 2.8 GW compared to a peak load of 1.9 GW. [24]

In February 2007, the governments of the three Baltic States and Poland agreed to build a new nuclear power plant at Ignalina—the Visaginas project. Lithuania passed a parliamentary bill in July 2007 calling for construction and completion by 2015. The Lithuanian government announced that it would conduct direct negotiations with potential investors and that it hoped to begin operation of the new plant in 2020. [25] This led to exclusive negotiations with Korean utility KEPCO, which turned down cooperation in early December 2010, two weeks after submitting a bid. In December 2011 Poland withdrew from the project [26].

The Lithuanian government, along with its partners in Estonia and Latvia, picked Hitachi together with its Hitachi-GE Nuclear Energy Ltd. unit as a strategic investor and technology supplier to construct a nuclear plant by the end of 2020. [27] In May 2012, the percentage breakdown of the initially $6.5 billion project were announced with a 20 percent ownership for Hitachi, and 38 percent for Lithuania, while Estonia would take 22 percent and Latvia 20 percent. [28]

However, in October 2012 a consultative national referendum on the future of nuclear power was held in Lithuania and 63 percent voted against new nuclear construction, with sufficient turnout to validate the result. [29] Prior to his appointment as Prime Minister, Algirdas Butkevicius, stated that legislation prohibiting the project would be submitted once the new parliament convenes and that “the people expressed their wish in the referendum, and I will follow the people’s will”. [30]

Renewable energy suppliers are making use of the current situation to promote their expansion. The Lithuanian wind energy association has stated: “The newly elected government will have to make a new energy strategy, where onshore and offshore wind power possibly could take the place of nuclear power”, both with a doubling of domestic production, to 500 MW and imports linked to wind development in Sweden and Poland. [31]

Remarkably a Lithuanian government commissioned report concluded that under both low and high gas price scenarios it would be cheaper to buy electricity from the regional market than to proceed with the construction of a nuclear reactor in the country. Consultants at the Lithuanian Energy Institute concluded that current costs of electricity, including imports, would be 4–10 Lithuanian cents (1.5–3.8 US cents) per kilowatt-hour less than power from a new reactor. Under these conditions it would save Lithuania $152.8 million per year not to build the reactor. [32]

Poland planned the development of a series of nuclear power stations in the 1980s and started construction of two VVER 1000/320 reactors in Żarnowiec on the Baltic coast, but both construction and further plans were halted following the Chernobyl accident. In 2008, however, Poland announced that it was going to re-enter the nuclear arena. In November 2010, the government adopted the Ministry of Economy’s Nuclear Energy Program, which was submitted to a Strategic Environmental Assessment. Poland aims to build 6 GW of nuclear capacity with the first reactor starting up by 2020. In response over 60,000 submissions were received from neighboring Germany; the results are due in the summer of 2013.

Officials have revised the planning in the meantime targeting 2022–23 for the startup of the first reactor. The State utility PGE set up two daughter companies to implement the project, which is supposed to result in two nuclear power stations with 3 GW capacity each. PGE announced the choice of three potential sites in December 2011: Gąski (Mielno), Lubiatowo (Choczewo) and Żarnowiec. Financing of the ambitious project remains unclear and public opinion is highly uncertain. While Poland was the only country showing a majority in favor of nuclear new-build in a 24-country opinion survey in June 2011 [33], a local referendum in February 2012 in Mielno showed a surprising 94 percent opposed to the plan. The Polish government reacted by starting a $6 million public information campaign, labeled “Meet the Atom”. “We want to make sure that the first Polish nuclear power plant is established with the approval of Polish society”, Hanna Trojanowska, vice minister and government commissioner for nuclear energy, stated in late March 2012. [34] The director of external relations for the state utility PGE, which promotes the project, stated that “obviously we will not proceed against the will of local people”. [35] A September 2012 update of the 24-country opinion survey identifies Poland as one in only three countries where public support for nuclear power decreased, from 61 to 53 percent. [36]

The project does not seem to be going forward very quickly, and in January 2013 the Polish utility PGE selected Australia’s Worley Parsons to conduct a five-year, $81.5 million study on the siting and development of a nuclear power plant, with a capacity of up to 3 GW. [37] The Polish government is reviewing the project and aims to streamline project management in order to reduce costs. It was foreseen that the first units will come into operation around 2023, with the last ones before 2030. A tender for construction and financing was to be opened in the end of 2013. But this schedule is likely to slip as the Prime Minister, Donald Tusk, stated in June 2013 that new nuclear may not be needed if shale gas is developed: ’I’m not ruling out nuclear in our energy mix, but later than planned (...) This is primarily due to the expected growth of natural gas as an energy source, including domestic shale gas.’ [38]

In August 2009 the Kingdom of Saudi Arabia announced that it was considering launching a nuclear power program, and in April 2010 a royal decree stated: ’The development of atomic energy is essential to meet the Kingdom’s growing requirements for energy to generate electricity, produce desalinated water and reduce reliance on depleting hydrocarbon resources.” [39] The King Abdullah City for Atomic and Renewable Energy (KA-CARE) has been set up in Riyadh to advance this agenda and to be the competent agency for treaties on nuclear energy signed by the Kingdom. It is also responsible for supervising works related to nuclear energy and radioactive waste projects. In June 2010 it appointed the Finland- and Switzerland-based consultancy firm Pöyry to help define a ’high-level strategy in the area of nuclear and renewable energy applications’ with desalination. In June 2011 the coordinator of scientific collaboration at KA-CARE said that it plans to construct 16 nuclear power reactors over the next 20 years at a cost of more than 300 billion riyals ($80 billion). The first two reactors would be planned to be online in ten years and then two more per year until 2030. [40]

However, according to a World Energy Council survey, “Saudi Arabia reported that using nuclear is still under consideration and that the WNA figures given above [16 reactors, 20 GW] are speculative.” [41] The assessment confirms reports that the KA-CARE nuclear proposal has still not been approved by the country’s top economic board, headed by King Abdullah. [42] In March 2013, it was reported that a KA-CARE official has said that a tender is now unlikely for another 7–8 years. [43]

Saudi Arabia has very large electricity expansion projects. It plans to double installed capacity to 100 GW by 2021, mainly through fossil fuels, but with a 10 percent renewable target by 2020. There is a $100 billion state spending commitment over the next ten years on renewables and nuclear combined. [44] Recent announcements tend to emphasize renewables; for example, 24 GW of renewable capacity (producing one-third of projected electricity use) is reportedly targeted by 2020 and 54 GW by 2032. A renewable-and-nuclear policy statement is expected later in 2013. [45]

However, these choices are not only about energy and economics. Senior Saudi Arabian diplomats have reportedly stated that “if Iran develops a nuclear weapon, that will be unacceptable to us and we will have to follow suit”, and officials in Riyadh have said that the country would reluctantly push ahead with their own civilian nuclear program. [46] Independent experts have suggested that the drive for civil nuclear power in the region is seen by some as a “security hedge”, and that “if Iran was not on the path to a nuclear weapon capability you would probably not see this [civil nuclear] rush”. [47] Concerns over nuclear non-proliferation have led the Canadian Government, in a briefing note, to conclude that the Kingdom “does not meet Canada’s requirements for nuclear co-operation”. [48]

U.S. firms are also currently excluded from any projects due to the lack of a nuclear co-operation agreement. The likelihood of an agreement being signed has been reduced recently with a speech by Hashim Yamani, head of the KA-CARE that the Kingdom was reluctant to willingly forgo enrichment and reprocessing [49].